The Highest Paying MBA Internships You Can Find

An MBA education can open the door to an astounding number of lucrative opportunities before you’ve even completed your degree. Many MBA interns are earning hourly wages unfathomable to the larger majority who spent their undergrad internships restocking break rooms and memorizing coffee orders, all for a whopping $0 per hour. Below, we’ve laid out the highest paying internships in some of the most common industries for MBAs.

Stats for MBA interns on Management Consulted dwarfed most other intern salaries. Though the reality of management consulting may lack the seedy glamor portrayed by Don Cheadle and Kristen Bell in House of Lies, these numbers are certainly compelling enough on their own to keep the attention of ambitious young interns.

Deloitte, a consistent top hirer of MBA’s according to Fortune, may be a top destination for MBA interns as well, if compensation is any indication. In 2016, MBA’s at Deloitte make an average of $11,380 per month for a ten-week internship, with the opportunity to receive full second year tuition reimbursement for returning interns. Depending on their goals, interests, and professional backgrounds, interns join a client service team in Deloitte & Touch LLP, Deloitte Tax LLP, Deloitte Risk and Financial Advisory, or Deloitte Consulting LLP.

Management Consulted put the average MBA intern salary at A.T. Kearney at a staggering $11,500 per month. A.T. Kearney offers a ten-week summer internship, during which interns will have unique experiences, such as a three-day opportunity in the middle of the summer to converge in a single location with all of the season’s interns. During these three days, students have the opportunity to network, socialize, and learn about the different facets of the company.

Outside of consulting, there are plenty of opportunities for MBA interns. It is no secret that some of the highest paying jobs out there are in tech. Luckily, there is a sizeable demand for MBA’s at tech companies.

Despite the recent, um, controversy surrounding Facebook’s security practices, the social networks interns are making out well. Facebooked topped Glassdoor’s list of Highest Paying Internships in 2017, with a median monthly salary of $8,000. The 12-week business internships offer frequent Q&A’s with higher-level employees and the opportunity to tackle real problems that face the social networking platform.

It would be remiss to talk about MBA’s in tech without mentioning Amazon, which is fast becoming one of the largest MBA tech recruiters. With a median monthly pay of $6,400, Amazon also made Glassdoor’s list of Highest Paying Internships in 2017. Keep in mind, this number is the median for all Amazon interns, and does not factor in MBA education, which would likely yield a much higher number. Interns are assigned a strategic project that provides the opportunity to contribute to solving a real business issue. Additionally, an internship with Amazon is often a foot in the door to a full-time career with the internet retail giant. Amazon’s website encourages MBA’s to apply, stating:

“You will have the autonomy to think strategically, make decisions, and drive significant impact to the customer experience and the business. To be successful, you must be passionate about the business, flourish in ambiguity, and demonstrate nimble leadership.”

Two Sigma Investments, a relatively young investment management company, has been getting a lot of press for its generous internship compensation. According to Business Insider, the $40 billion hedge fund, which started in 2001, grew 400 percent from 2012-17. The 10-week internships can pay upwards of $10,500 per month. Internships at Two Sigma are primarily in STEM, and MBA’s with an interest in Quantitative Research might find this program particularly rewarding.

Cornell FinTech Disruption, Crowd-Funding Wisdom, and More – New York News

Let’s explore some of the most interesting stories that have emerged from New York City business schools this week.

Fintech is Disrupting the Disruptors, and We’re Ready For It – Johnson School of Management Blog

S.C. Johnson Graduate School of Management MBA candidate Arjun Devgan, ’18, highlighted how FinTech inventions such as cryptocurrencies, peer-to-peer lending, and smart insurance have begun to disrupt a post-PayPal landscape, which at one point disrupted traditional banking.

Devgan writes about two Cornell Tech intensives designed to “equip students to solve business problems in this age of digital transformation:” the digital marketing intensive and the fintech intensive.

“With my background in payments and remittances, the fintech intensive program offered me a launchpad to dive deep into the world of financial technology. Classes such as the Fintech Practicum, Business Models, Cryptocurrencies, and a Field Project with one of Citi Ventures’ portfolio companies offer a great combination of basic theoretical concepts and real-world experiential learning.”

Learn more about Johnson’s FinTech and Digital Marketing Intensives here.

Want People to Fund your Kickstarter Project? Sell Them on Your Reputation First – Binghamton School of Management Blog

Binghamton School of Management associate professor Ali Alper Yayla presented a new paper at the 51st Hawaii International Conference on System Sciences, which found that potential Kickstarter backers are more concerned about a producer’s “ethical characteristics than their actual ability to make and deliver the product.” Professor Yayla writes:

“We found that people worry more about the seller’s honesty than whether the seller actually has the ability and knowledge to finish and deliver on the product. People don’t want sellers to just take their money and run. Crowdfunding is interesting because you’re literally buying something that isn’t finished from a person who has never made it before. There are no product reviews, and there are no seller reviews.”

Read more about Yayla’s research here.

Can Mark Zuckerberg Fix Facebook’s Mess? – Forbes

In Len Sherman’s recent Forbes article “Can Mark Zuckerberg Fix Facebook’s Mess?”, the Columbia Business School executive in residence and adjunct professor noted the company’s seemingly astounding naivety of how much information was secretly (or not so secretly) being scrubbed for use by third party companies like Cambridge Analytica.

“It’s been hard to fathom how a company reputed to be run by one of the world’s most brilliant digirati, could have been so naïve in not recognizing the risks in giving outside developers broad access to Facebook’s user data, so lax in failing to ensure that rogue data in malevolent hands was destroyed before it could be weaponized, and so reluctant to advise users that their personal information was (and still is) floating around cyberspace. In short, what was Mark Zuckerberg thinking?”

Sherman theorizes that part of the issue is Zuckerberg’s sincere overconfidence that technology and innovation can only be used for a greater good, rather than being possibly manipulated by less-than-ideal forces. This, Sherman continues, was all done despite a litany of data that proved Facebook’s nefarious actors and less-than-strict partnerships were actively making the platform less safe year by year.

Click here to see the rest of Sherman’s work with Forbes.

What They’re Saying: The Facebook Fallout

It seems puzzling to say a company that is worth nearly half a trillion dollars is venturing somewhere near zero degrees Kelvin, but if you were only reading headlines this week you’d get the sense that Facebook isn’t looking so hot.

Since the break of the Cambridge Analytica scandal, the tech giant lost an estimated $100 billion USD in value, and its beleaguered founder Mark Zuckerberg lost an estimated $14 billion of his own worth. Fortunately for him, according to CNN, he’s still worth over $60 billion so he can easily afford more mayonnaise and butter sandwiches.

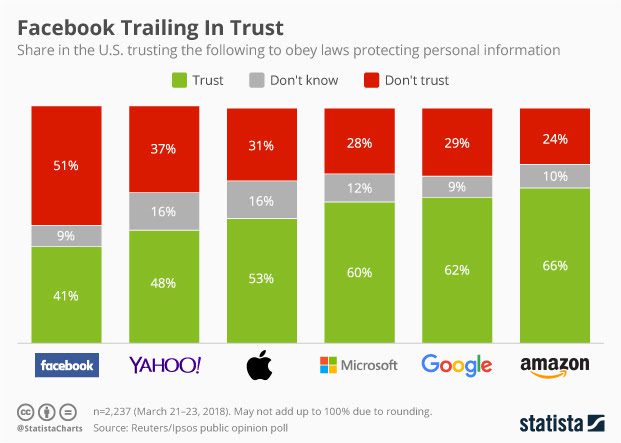

But the fallout is more than monetary. Trust in the social media company is at a critical low point, according to Statista data.

Janina Conboye at the Financial Times recently asked how the company may go about repairing its own image in “The MBA view: can Facebook fix its reputation?,” speaking with numerous business school faculty members, including London Business School‘s Jill Schlechtweg, who plainly says, “It is worth wondering whether Facebook can regain credibility at all. Arguably Mark Zuckerberg has evaded responsibility for the social costs of social media addiction, the proliferation of fake news, and now leaks of personal data for political ends.”

Check out how other business schools and industry experts are reacting the ongoing Facebook story below.

What @facebook knows about you apparently includes data about phone calls and messages. The revelation could make Facebook’s huge data scandal hurt more than ever. https://t.co/jActrbEB5i

— MIT Tech Review (@techreview) March 27, 2018

PSA: “Harvard Business School Prof. Shoshana Zuboff calls it “surveillance capitalism.” And as creepy as Facebook is turning out to be, the entire industry is far creepier. It has existed in secret far too long…” https://t.co/vSPlAyWnzu

— Mitchell Schneider (@Mitski) March 27, 2018

What Cambridge Analytica is accused of doing, Facebook and Silicon Valley giants like Google do every day, indeed, every minute we’re logged on. – https://t.co/8O9730vddo

— Mark Schaefer (@markwschaefer) March 29, 2018

In the wake of the Cambridge Analytica scandal, Apple is making their position clear on privacy. https://t.co/OLIl5ihtby

— FOX MBA & MS (@FoxMBA) March 28, 2018

.@profgalloway weighs in on #Facebook‘s handling of the Cambridge Analytica scandal via @barronsonline https://t.co/6zWqfAa3nk

— NYU Stern (@NYUStern) March 28, 2018

How a Rutgers Part-Time MBA Led to a Dream Job, and More – New York News

Let’s explore some of the most interesting stories that have emerged from New York City business schools this week.

Part-Time MBA Proves to be a Steppingstone to Dream Job – Rutgers Business School

From running phone sales in Manhattan, to working her way up the corporate business to business ladder, Allegra Kipnis, a part-time MBA candidate from the Rutgers Business School in New Brunswick, found her “dream job.”

In a recent profile with the school, Kipnis divulged that earning her MBA helped her earn multiple promotions with Verizon. But, even after being let go, she (with the help of the Rutgers community) helped her refine her career path on the way to a dream role with Panasonic as an internal communications specialist.

“The MBA program gave me the tools I needed to eventually land my dream job, but funny enough, after all I had learned, it turned out to be just one more step in the story of my career,” she said in the interview.

Kipnis, a part-time MBA candidate at Rutgers / photo via Rutgers.edu

You can more about Kipnis’ career path and the Rutgers Business School part-time MBA program here.

A Combination of Personality Traits Might Make You More Addicted to Social Networks – Binghamton School of Management

The Binghamton University School of Management recently published new research, “Personality Predictors of IT Addiction,” in which assistant professor of management information systems Isaac Vaghefi, along with DePaul’s Hamed Qahri-Saremi, examined which collection of personality traits often leads to social networking addiction among 300 college-aged students: neuroticism, conscientiousness, and agreeableness. Vaghefi writes:

“It’s more of a holistic approach to discover what kind of people are more likely to develop an addiction. Rather than just focusing on one personality trait, this allows you to look at an all-inclusive personality profile.”

Read more about the duo’s research here.

Admissions Bridge Connects Diverse Undergraduates to MBA Possibilities – Johnson School of Management Feed

The SC Johnson School of Management blog recently published an overview of the school’s second annual Johnson Admissions Bridge—an event that encourages “undergraduate women and students from underrepresented backgrounds at Cornell to consider business school and discover ways to begin preparing now.”

The Bridge is “part of a larger initiative to ensure a diverse population is offered the opportunity to attend business school.” Judi Byers, executive director of admissions and financial aid at Johnson, explains:

“At Johnson, we have both an opportunity and a responsibility to contribute to the pipeline of diverse talent ultimately seeking entry into top business schools and the companies and organizations they will lead afterward. The Bridge is a way to connect with our undergraduate students here at Cornell and gives us the chance to talk with them about potential career paths and how an MBA might offer value to their short and long term career goals.”

Learn more about the Cornell Bridge here.

What They’re Saying: Business Schools Talk About Cambridge Analytica

Less than a week after Christopher Wylie, the whistle-blower in the ongoing Cambridge Analytica controversy, helped reveal the “dirty tricks” the data mining firm used to help swing elections in North America, Europe, and Africa—including the 2016 U.S. general election—business schools are reacting to the dynamic story.

In short, UK television outlet Channel 4 News filmed several Cambridge Analytica members in an undercover operation, in which they revealed numerous strategies, including: soliciting fake bribes, hiring prostitutes to seduce potential candidates in elections, and more. Company chief executive Alexander Nix was also filmed in the video, which you can watch here, boasted the company’s outreach methods on social media, saying: “It sounds a dreadful thing to say, but these are things that don’t necessarily need to be true as long as they’re believed.”

Another member of the Cambridge Analytica team also argued that they constructed President Donald Trump’s popular “crooked Hillary” campaign slogan from 2016.

Further, the controversy revealed how the company pilfered upwards of “50 million” Facebook profiles, most of which came without consent. Facebook and its founder Mark Zuckerberg played silent on the ongoing story up until March 21, plainly saying in a CNN interview “I’m really sorry that this happened.”

“Aleksandr Kogan, the data scientist who passed along data to SCL Group and its affiliate Cambridge Analytica, built a Facebook app that drew data from users and their friends in 2013. He was allowed access to a broad range of data at the time.

Though Kogan’s data was properly obtained, he breached Facebook’s policy when he shared that information with a third party, Facebook has said. When Facebook learned about the information being shared, it asked Cambridge Analytica to destroy the data. Cambridge said it had.”

Wylie notes that Cambridge Analytica probably never destroyed that data, inevitably leading towards the company’s involvement in the 2016 election. Several of the nation’s most prominent business schools talked about the story on Twitter, which you can read below.

André Spicer, Professor of Organisational Behaviour, on Cambridge Analytica and the possibility of tech companies being forced to expand regulations on privacy and social responsibility.

Read André’s comments: https://t.co/O5IAlUTD5t#cambridgeanalytica#cassbusinessschoolpic.twitter.com/GWv95RUIMc

— Cass Business School (@cassbusiness) March 21, 2018

“The really big issue is if regulators start questioning the business model of tech firms. Currently, consumers give away their data in exchange for free services, but what if regulators start putting a price on people’s data?” –

Cass Business Professor André Spicer

Q&A with @cyberlawclinic‘s @vivekdotca about Facebook and Cambridge Analytica, U.S. privacy protections, and the regulation of the tech industry https://t.co/LPKwwSKSXw

— Harvard University (@Harvard) March 22, 2018

The head of the European Parliament announced on Monday that the EU will investigate whether the data of more than 50 million Facebook users were misused when it was accessed by Cambridge Analytica! https://t.co/q946Hed417

— FOX MBA & MS (@FoxMBA) March 22, 2018

Cambridge Analytica said it’s suspending its CEO immediately and is launching an independent investigation into allegations it misused data on millions of Facebook users. https://t.co/EKeXiuHeQF

— MIT Tech Review (@techreview) March 21, 2018

Boston News: Northeastern Explores Trump Tweets, MIT Offers FinTech Advice and More

Let’s explore some of the most interesting stories that have emerged from Boston metro business schools this week.

Can A Trump Tweet Dramatically Sway A Company’s Value? – Northeastern’s D’Amore-McKim Blog

Will Clark, DMSB ’17, along with Northeastern University D’Amore-McKim School of Business finance professors David Myers and Jeffery Born, sought to understand the impact that President Trump’s tweets—which often directly address publicly traded companies like Ford, Toyota, Walmart, GM, and Boeing—had on their stock market value.

“Past presidents communicated through the media. This was the first time that a president was communicating directly with the public—with investors—about companies. We really weren’t sure what to expect from the data,” says Clark, who is now a credit analyst with Morgan Stanley.

The trio’s research found that Trump’s tweets, in fact, did have some impact on companies, often increasing trade volume within the first few hours and days after he references them on the social media platform. The research was revealed in the academic journal Algorithmic Finance.

“The team found that Trump’s tweets dramatically increased trading volume for the companies’ stocks in the first few days following a tweet. They also found that positive (or negative) tweets about companies increased (or decreased) the firms’ stock prices by a modest amount—just 1 percent. But the changes were only temporary: Within a few days, the firms’ trading volumes and stock prices returned to pre-tweet levels.”

The lasting effect, however, was found to be longing. The trio notes that the most active traders, which they refer to as “noise traders,” were very reactive to Trump’s words, with trading tapering off after only a few days.

“They’re regular people and under-informed investors who want to get in and out and make a buck without thinking too long and hard about it,” Born notes about the financial impact of Trump tweets.

You can read more about the financial research on the Trump tweets from D’Amore-McKim here.

3 Lessons To Keep In Mind When Starting A FinTech Venture – MIT Sloan Newsroom

MIT Sloan School of Management MBA alum Sophia Lin, ’12, and her partner Andrew Kelley of the FinTech startup Keel, which connects “rookie investors with more seasoned ones,” shares some hard-won lessons in an op-ed for the Sloan blog. First of all: beware of hidden costs specific to FinTech. “

“Starting costs are higher than other industries because of data, infrastructure, and security requirements,” Lin said. “Data is expensive, which stops a lot of early stage startups from entering this field. But you need data to build your product.”

Read all of Lin’s words of wisdom here.

More CEOs Have Begun To Take Social Responsibility Seriously – HBR

CEOs from Facebook’s Mark Zuckerberg to Blackrock’s Larry Fink have begun to take very public stands to address the long-term impacts their products have had and continue to have on communities and the environment.

“We are witnessing a big, transitional moment—akin to the transition from analog to digital, or the realization that globalization is a really big deal. Companies are beginning to realize that paying attention to the longer term, to the perceptions of their company, and to the social consequences of their products is good business.”

Harvard Business School John and Natty McArthur University Professor Rebecca M. Henderson also explains that there are distinct differences between the size of a company, which often contrasts with the social goals of the company. The larger the company, the more long-term the outlook, she explains. Unlike small companies, larger firms worry about quarter-to-quarter results less.

“Big firms can also internalize certain externalities. An externality is a cost from a transaction that doesn’t fall on the buyer or the seller. If I pollute the air to make a product I sell to you, the cost of that pollution is spread out across society, and isn’t incorporated in the price I charge you for the product. Externalities pose problems for markets, since neither buyer nor seller have any incentive to deal with the costs. But sometimes, for really large firms, things work differently.”

The unfortunate causality, she notes, is that we are often reliant on the largest companies to take the initiative for causes that may be considered part of the global good. If some companies among the Fortune 500 elect to, say, go carbon neutral within the next decade, that can have a profound impact on other competing companies. And if those initiatives are not as profitable, there is an even greater risk of other companies being reluctant to attempt similar efforts.

Read more about the growing CSR trend among CEOs here.