Columbia Business School Announces New M.S. in Business Analytics Degree

Columbia Business School (CBS), together with Columbia Engineering, yesterday announced a new full-time Master of Science in Business Analytics degree. Distinct from CBS’s MBA degree, the new program features a three-semester curriculum and is really geared toward students who want to learn the modeling techniques and data science tools that help businesses use data to influence decision making. A unique capstone project will serve as a key element of the new program, through which students will work with actual clients and relevant data sets to put the skills they’ve learned to work helping solve those companies’ real-world business problems. The capstone course will extend over the full three semesters of the program.

The program was developed jointly by faculty at both CBS and Columbia Engineering, and the resulting curriculum is designed to prepare graduates to excel in careers both as consulting analysts and associates and as business analysts and data scientists in fields including financial and professional services, technology, advertising and media, and other professions that require both a deep understanding and practical application of data analytics.

“By tapping into the vibrant and diverse business ecosystem that can only be found in New York, Columbia Business School and Columbia Engineering are uniquely situated to offer this new Master’s degree,” CBS Dean Glenn Hubbard said in a statement. “We see this as a must-do program for any future business person who wants to have a leg up in using data to make informed business decisions.”

CBS Enters an Already Crowded Field

Columbia is far from the first to announce a new data analytics master’s program—and it likely won’t be the last. It joins a long and growing list of other leading business schools that have sensed demand from both students and recruiters for programs that marry some of the skill sets of the MBA with the deeper study of data science and analytics that engineering faculty can provide.

MIT Sloan School of Management last year launched its own Master of Business Analytics (MBAn) degree, with leadership and support from the MIT Operations Research Center. In just one year, applications to the program have more than doubled—from 300 to 800—making the degree the most competitive at the school, with an admissions rate of less than 4 percent, the school reports. And just last month Sloan unveiled a new Business Analytics Certificate program that will be open to students in all MIT masters-level programs who want more rigorous academic content focused on data science.

Not to be left out, last month the University of Virginia’s Darden School of Business announced the launch of a new MBA+MSDS dual-degree program, which grants a Master of Data Science degree from UVA’s Data Science Institute and an MBA from Darden in 24 months (tuition for the MBA+MSDA program is the sum of each individual program’s standalone tuition). The program welcomed a pilot cohort this past summer, and Darden is currently accepting applications for the full program, which will launch in 2018.

NYU Stern, for its part, is now accepting applications for the inaugural class of a new specialized one-year Tech MBA, first announced last spring. And just yesterday Stern shared that an $8 million alumni gift will fund creation of a new center for technology, business, and innovation.

YOU MIGHT ALSO LIKE: More Business Schools Training MBA Students for Careers in Tech

Harvard Business School (HBS), too, sees where the action’s at and doesn’t intend to sit idly on the sidelines. In August 2017—together with the Harvard John A. Paulson School of Engineering and Applied Sciences and the Faculty of Arts and Sciences—HBS announced a partnership with 2U, Inc. to deliver a new online certificate program in business analytics. Expected to welcome its first cohort of students in March 2018, the Harvard Business Analytics Certificate Program is designed to help business leaders—including MBA grads—keep up with and leverage the explosion of data now available in every industry.

Some Schools Were Out in Front

Of course, amid this recent flurry of activity to enhance academic offerings at the intersection of technology and business, some schools can claim clear first-mover advantage. MBA students at CMU’s Tepper School of Business can opt to pursue a Technology Leadership MBA Track, a joint partnership between the Tepper School and Carnegie Mellon’s top-ranked School of Computer Science—indeed, it is one of the most popular offerings in the MBA program. Tepper also offers a three-year, dual-degree MBA/Master of Software Engineering program, also in partnership with the School of Computer Science.

And Stanford Graduate School of Business has for several years offered its students the opportunity to pursue a dual degree of significant relevance to students interested in careers in tech. Its joint MA in Computer Science/MBA degree links two of the university’s world-class programs and helps students develop a unique skill set ideal for becoming a manager and/or entrepreneur for new technology ventures. Stanford’s program includes a year of courses at each the GSB and in the Computer Science department followed by a third year of elective courses in both programs, enabling students to shave off one to two semesters it would take to complete both degrees separately.

RELATED: Best Business Schools to Jumpstart Your Career in Tech—Or Advance It

It Only Makes Sense

Whether beginning several years ago or just getting off the ground now, that business schools are recognizing and responding to market demand for business fundamentals married with data science know-how makes complete sense.

“The role of analytics has grown increasingly critical for most sectors of the economy,” Columbia Engineering Dean Mary C. Boyce said in a press release. “Our partnership with Columbia Business School combines our strength in data science, optimization, stochastic modeling, and analytics with their strength in data-driven decision-making for business and marketing to create a rigorous new master’s degree program.”

What Sets Columbia’s New Program Apart?

So what sets the newest program announced yesterday by Columbia apart from others in a crowded field? One distinguishing feature of the M.S. in Business Analytics is the capstone project that will put students to work on real-life consulting projects with companies using the companies’ own data, the school argues. “By working on real-world consulting projects, with real-world data, students will use the modeling techniques and data science tools to provide pragmatic solutions to the practical problems that businesses are facing today,” Costis Maglaras, professor and chair of CBS’s Decision, Risk & Operations Division, said in a press release.

Students in the new Columbia Business analytics degree program will also have valuable access to dedicated career placement services, the school notes, starting with completing a required Professional Development and Leadership course. “The M.S. in Business Analytics combines classroom instruction by distinguished Columbia professors with the experience of working on real-world problems via the capstone project course,” Columbia Engineering Professor Garud Iyengar said in the press release. “We expect this program to have 100 percent placement of its graduates as do our very successful M.S. in Management Science and Engineering and M.S. in Financial Engineering programs.”

Applications are currently being accepted for the first cohort of this new M.S. in Business Analytics. Students can choose to complete the program in one year by taking a summer semester or can take three non-contiguous semesters (fall, spring, fall), which would reserve the possibility of a summer internship.

For more information about the new Columbia M.S. in Business Analytics, click here.

This article has been edited and republished with permissions from our sister site, Clear Admit.

Harvard Offers Strategies For Getting Support to Develop New Skills on the Job

Rachel O’Meara, Google Sales Executive, Leadership Coach, and Pause author, recently wrote for Harvard Business School‘s Harvard Business Review, offering six effective strategies to convince your current employer to help you develop new skills on the job.

- Identify how you want to learn and grow. “Spend time honing in on exactly what you need. Write down what you want to learn and how you would grow from the experience you’ve identified. The more you can write down, the more aware and real your ideas become.”

- Own it. “Rather than being embarrassed or nervous about asking for time to build an underdeveloped skill, own it as part of your commitment to becoming a better leader.”

- Create your vision statement. “Visions are a great way to orient and stay on track before, during, and after your development work. In one sentence, answer the question: Who will I become as a result of this investment of my time and resources?”

- Connect your goals or outcomes to what the business needs. “To get buy in to support your development, you have to connect…what specific skills or knowledge you can share from your training or experience. Are there issues at work that you could better resolve as a result of this training? In what ways will your company benefit from your improved performance, skills, or knowledge?”

- Prep and practice. “Make a list of what is negotiable – things like timing, budget, and activity. When preparing for the conversation, think about what each person involved in making the decision has to gain. Do your homework and read up on your HR policies.”

- Make your ask. “When you’re ready to sit down with your manager, don’t catch them off guard. Give them ample notice and consider adding it to the agenda for your next one-on-one meeting.”

O’Meara concludes: “There are three likely outcomes: getting what you’ve asked for, getting some of what you asked for, or getting a flat out “no.” By following these steps, you’ll increase the chances that you get a favorable outcome, but that’s not always the case. Even if you don’t get what you asked for, start thinking about ways you can reshape your request in the future.”

Harvard Explores How Independent Bookstores Have Stuck Around in the Amazon Era

Amazon may slowly be turning the small consumer business world into a Mad Max-ian wasteland, but brick-and-mortar bookstores are still somehow enduring, writes Harvard Business School.

Ryan Raffaelli, an Organizational Behavior professor at HBS and field researcher whose work is inspired by stories of “technology reemergence,” including the recent reinvention of the Swiss watch industry, has prepared a new abstract due for publication in 2018, “Reframing Collective Identity in Response to Multiple Technological Discontinuities: The Novel Resurgence of Independent Bookstores.”

Raffaeli examined how, after a nearly two-decade-long plummet, independent bookstores staged an unprecedented comeback between 2009 and 2015 after “Amazon forced Borders out of business in 2011.” This was also due in no small part to the efforts of the American Booksellers Association (ABA), which facilitated “partnerships between bookstores and other local businesses and strengthened the collective identity of indie bookstores by helping its members share best practices, such as how to use social media to promote special events.”

Raffaeli explains, “This has been an especially fascinating industry to study because indie booksellers provide us with a story of hope.”

Over 200 bookstore owners, publishers, and authors across 13 states were surveyed and the results were consolidated into the “3 C’s of independent bookselling’s resurgence community, curation, and convening.”

Community: “Bookstore owners across the nation promoted the idea of consumers supporting their local communities by shopping at neighborhood businesses [and] stressing a strong connection to local community values.”

Curation: “Independent booksellers began to focus on curating inventory that allowed them to provide a more personal and specialized customer experience.”

Convening: “Independent bookstores have become intellectual centers for convening customers with likeminded interests—offering lectures, book signings, game nights, children’s story times, young adult reading groups, even birthday parties.”

“The theoretical and managerial lessons we can learn from independent bookstores have implications for a wide array of traditional brick-and-mortar businesses facing technological change.”

Harvard Business School Research Offers New Spin on “Time Is Money” Axiom

Money can buy happiness, according to recent research from the Harvard Business School. But, it primarily has to be spent on making time.

Ashley Whillans, an Assistant Professor of Business Administration at HBS, published research on the “impact of buying one’s way out of negative experiences,” whether that means find ways to reduce a commute or taking a vacation. She points to “time stress”—or the tension that arises when time becomes a scarce resource—as a critical source of unhappiness, especially for many wealthy individuals. She explains:

“People have been trying to find ways to use their discretionary income to maximize their quality of life for a long time. We were really interested in seeing if buying ourselves out of negative experiences might be another pathway to happiness that had been relatively unexplored.”

For the purposes of their research, Whillans and her team define happiness as both overall and moment-to-moment satisfaction.

Whillans surveyed American, Canadian, Danish, and Dutch citizens across the socioeconomic spectrum about their feelings after they made a time-saving purchase. All participants generally reported positive feelings after ordering take-out food, for instance, but Whillans found that when they made these purchases too often, consumers developed a type of “hedonic adaptation” where they used the extra time to do something pleasurable rather than productive.

The role of gender in the time/money/happiness equation is notable, particularly when it comes to the post-work childcare and housekeeping “second shift” many American and Canadian women have to pull. The result is that women “have more educational opportunities than before, and [are] likely to be making more money and holding high-powered jobs but their happiness is not increasing commensurately.”

In ongoing research Whillans is pursuing with Michael Norton, a Harold M. Brierley Professor of Business Administration, into the influence that time-saving purchases have on relationship satisfaction, she explains that “both men and women feel less pulled between the demands of work and home life, and that positively impacts the relationship.”

Whillans’ research offers tangible proof that outsourcing specific tasks throughout the week is a fiscally responsible way to relieve stress.

Check out the rest of Harvard Magazine’s story on the research here.

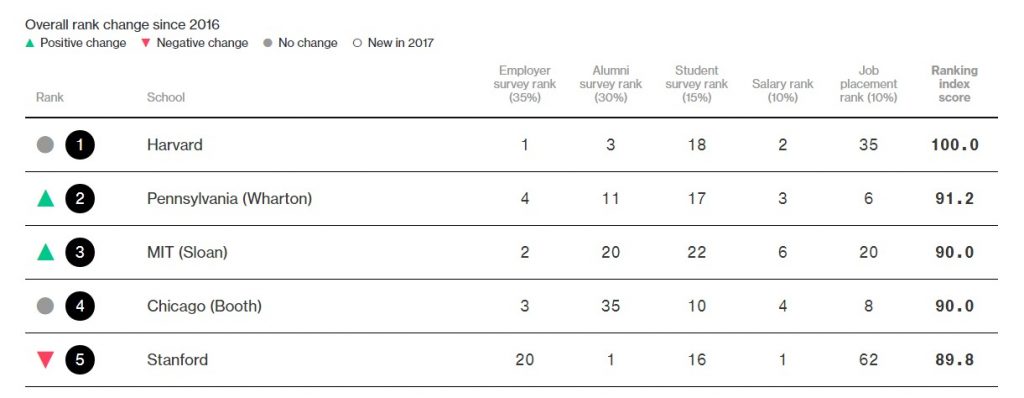

Harvard Business School Tops Bloomberg Businessweek Ranking

For the third straight year, Harvard Business School reigned supreme in the annual Bloomberg Businessweek “Best Business Schools” ranking, topping the Wharton School at the University of Pennsylvania and MIT Sloan School of Management. In joining HBS on the medals podium this year, those schools both saw significant gains over last year, climbing from sixth and seventh respectively.

Rounding out the top five this year is the University of Chicago Booth School of Business —holding steady year over year at fourth—and Stanford Graduate School of Business, which fell from second place in 2016 to fifth this year.

The methodology Bloomberg Businessweek uses to arrive at its annual MBA ranking involves weighting each of five principle factors. Employer surveys account for 35 percent of a school’s score. Alumni surveys account for another 30 percent. And a combination of current student surveys, salary rankings, and job placement together account for the remaining 35 percent of the final score.

High Risers

Ten out of the top 20 ranked schools in the 2017 Bloomberg Businessweek ranking advanced at least one spot over last year. Wharton and Sloan each managed to leap four spots, boosted by high praise from employers and hefty salary benefits for recent graduates. The University of Washington Foster School of Business also managed to jump from 19th to 15th overall this year, thanks largely to its top ranking as the nation’s best business school for job placement.

The Cornell S.C. Johnson Graduate School of Management and the UCLA Anderson School of Management both saw a rankings jump of three spots, with Johnson moving up to 13th and Anderson coming in at 19th.

The year’s biggest winner, however, may be the Penn State Smeal College of Business, which jumped a whopping 12 spots from last year’s 37th to come in at 25th in 2017. It wins the award for the year’s biggest overall rankings increase. The USC Marshall School of Business also saw a momentous climb this year, sidling up eight spots from 38th last year to 30th this year.

In the latter half of the rankings came another one of this year’s biggest risers, with the Terry College of Business at the University of Georgia jumping 11 spots from last year, up from 65th overall to 54th. Elsewhere, the David Eccles School of Business at the University of Utah, the Whitman School of Management at Syracuse University, the C.T. Bauer College of Business at the University of Houston, and the Pepperdine University Graziadio School of Business and Management all saw a jump of at least seven spots in the new ranking.

Once Mighty, Now Fallen

Stanford GSB, Duke’s Fuqua School of Business, Dartmouth’s Tuck School of Business, and Jones School of Business at Rice University may all be feeling a wee bit dizzy. Last year Stanford shot up to second from seventh the year before, but this year it finds itself demoted to fifth. Duke’s Fuqua School, which last year celebrated a momentous jump from eighth to third, this year fell back down to seventh. Dartmouth’s Tuck School of Business, which had one of last year’s biggest gains, rocketing up nine spots to break into the top five from a mere 14th place finish the year before, this year finds itself at seventh. Similarly, Rice Business, as the Jones School likes to be called, which last year catapulted 11 spots to number eight, this year slipped to tenth. But at least all maintained their footing within the top 10.

Emory’s Goizueta Business School and the Texas A&M Mays Business School, for their part, slipped out of the top 20 altogether. Goizueta slipped just slightly, from 20th to 21st, and Mays slid from 18th to 22nd. The University of Virginia Darden School of Business also stumbled, slipping from 12th last year to 17th this year. But the Charlottesville school at least managed to remain in the top 20, thanks in part to strong scores in the student survey and salary categories.

No school, however, lost more ground than the George Washington University School of Business, which fell an eye-popping 14 spots from last year, losing its place among the top 50 business schools in the United States.

Bloomberg BW has made multiple changes to its methodology in recent years, resulting in significant volatility in terms of where schools fall on the list even when not much has changed year over year at the individual schools themselves. This has led many to question the credibility of the ranking overall. That said, Clear Admit’s Alex Brown found this year’s results easier to swallow than some in recent years. “This ranking seems more reasonable to me this year,” he says. “Each of the M7 programs are in the top 10, and the schools I would consider in the top 16 are all in the top 20.”

You can view the complete 2017 Bloomberg Businessweek rankings here.

This article has been edited and republished with permissions from Clear Admit.

How Boston Business Schools Help Low-Income MBA Applicants

Anyone planning on earning a postgraduate business degree knows that MBA programs cost a lot of money. In the Boston metro, where the cost of living is already high, the annual cost of an MBA program can reach upward of $100,000 … Ouch! Continue reading…