What They’re Saying: Business Schools Talk About Cambridge Analytica

Less than a week after Christopher Wylie, the whistle-blower in the ongoing Cambridge Analytica controversy, helped reveal the “dirty tricks” the data mining firm used to help swing elections in North America, Europe, and Africa—including the 2016 U.S. general election—business schools are reacting to the dynamic story.

In short, UK television outlet Channel 4 News filmed several Cambridge Analytica members in an undercover operation, in which they revealed numerous strategies, including: soliciting fake bribes, hiring prostitutes to seduce potential candidates in elections, and more. Company chief executive Alexander Nix was also filmed in the video, which you can watch here, boasted the company’s outreach methods on social media, saying: “It sounds a dreadful thing to say, but these are things that don’t necessarily need to be true as long as they’re believed.”

Another member of the Cambridge Analytica team also argued that they constructed President Donald Trump’s popular “crooked Hillary” campaign slogan from 2016.

Further, the controversy revealed how the company pilfered upwards of “50 million” Facebook profiles, most of which came without consent. Facebook and its founder Mark Zuckerberg played silent on the ongoing story up until March 21, plainly saying in a CNN interview “I’m really sorry that this happened.”

“Aleksandr Kogan, the data scientist who passed along data to SCL Group and its affiliate Cambridge Analytica, built a Facebook app that drew data from users and their friends in 2013. He was allowed access to a broad range of data at the time.

Though Kogan’s data was properly obtained, he breached Facebook’s policy when he shared that information with a third party, Facebook has said. When Facebook learned about the information being shared, it asked Cambridge Analytica to destroy the data. Cambridge said it had.”

Wylie notes that Cambridge Analytica probably never destroyed that data, inevitably leading towards the company’s involvement in the 2016 election. Several of the nation’s most prominent business schools talked about the story on Twitter, which you can read below.

André Spicer, Professor of Organisational Behaviour, on Cambridge Analytica and the possibility of tech companies being forced to expand regulations on privacy and social responsibility.

Read André’s comments: https://t.co/O5IAlUTD5t#cambridgeanalytica#cassbusinessschoolpic.twitter.com/GWv95RUIMc

— Cass Business School (@cassbusiness) March 21, 2018

“The really big issue is if regulators start questioning the business model of tech firms. Currently, consumers give away their data in exchange for free services, but what if regulators start putting a price on people’s data?” –

Cass Business Professor André Spicer

Q&A with @cyberlawclinic‘s @vivekdotca about Facebook and Cambridge Analytica, U.S. privacy protections, and the regulation of the tech industry https://t.co/LPKwwSKSXw

— Harvard University (@Harvard) March 22, 2018

The head of the European Parliament announced on Monday that the EU will investigate whether the data of more than 50 million Facebook users were misused when it was accessed by Cambridge Analytica! https://t.co/q946Hed417

— FOX MBA & MS (@FoxMBA) March 22, 2018

Cambridge Analytica said it’s suspending its CEO immediately and is launching an independent investigation into allegations it misused data on millions of Facebook users. https://t.co/EKeXiuHeQF

— MIT Tech Review (@techreview) March 21, 2018

Joe Biden Talks Industrialization, Income Inequality at Northwestern Kellogg

On March 9th, an eager audience gathered at Northwestern University’s Kellogg School of Management to hear what wisdom Joe Biden might have to impart from his distinguished political career to the world of business.

Speaking the day after observations of International Women’s Day around the world, the former vice president opened his talk with with a message about inclusion. He cautioned the crowd that “in order for a country to succeed… it has to husband all its assets. It cannot leave half its initiative, half its brain power, half of its courage, half of its capability, half of its strive behind.”

Although it was only a preface, the call for gender equality set the tone for the rest of the speech. The overarching theme, in Biden’s words, was inequity. And he didn’t just discuss the wage gap; he focused on what he called “geographic inequity,” or the rising inequality between various American cities and towns.

For much of his time at the podium, Biden decried the recent fate of industrial America, and of the middle class. He gave a bleak description of once-thriving Midwest towns and cities: “It’s called depression,” he said. “Empty factories, empty storefronts, empty homes, empty wallets. And the underpinnings of this geographic inequity are no mystery. It’s been in the making for years. States, and state laws, have undercut organized labor and the right to bargain, stunting the movement. The labor movement has been hollowed out and good, middle class jobs have been lost.”

Biden went on to discuss the disparity between cities on the coasts and those in the Midwest, saying that “a poor child in San Francisco has twice the chance of making a top income than one born in Detroit or Wilmington or Saginaw.”

He concluded that this is due to the fact that “they come from less segregated communities. There’s less income inequity, allowing them to see success around them. Their school systems are better funded. Social networks are stronger. More people are taking part in their communities.”

The talk was framed by current political issues, and the general solution that Biden gave spoke directly to the audience, comprised of MBA students and faculty. The major takeaway of the speech was that business leaders—those who will go on to shape the economy and, to some extent, policy—have a social responsibility.

He emphasized the importance of work, not just for economic stability, but as a source of identity. Biden recounted his father telling him, “Joey, you gotta remember a job’s about a lot more than a paycheck. It’s about your dignity, it’s about your respect, it’s about your place in your community. I mean this literally, not figuratively.”

As an example, he brought up causal links between unemployment and other social ills. For instance, he added that “every one percent increase in unemployment raises opiod deaths in a community by four percent.”

For Biden, the social obligation to push for fair wages and workers’ rights is not just about raising morale. Rather, it is central to the spirit of capitalism. The role that the business community must play in this scenario, according to Biden, is to push back against policies that limit workers’ rights.

Students at Northwestern Kellogg during the Biden speaking event. Photo via Evan Garcia / Chicago Tonight

Making sure that workers earn wages that match their productivity is a necessary part of a healthy economy. And, by extension, a healthy economy produces and furthers a healthy society.

Biden identified a few common business practices that he described as both anti-labor and anti-competition. He posed a rhetorical question to the audience: “The capitalist system, I thought—and I’m a capitalist—is all about being able to compete and bargain. So how do you justify non-poaching agreements to prevent one franchise from hiring away workers from another franchise?”

He added, “How do you justify taking hourly wage-earners, not managers at all, and re-classifying them, denying them in 1.2 billion dollars in wages, to go to shareholders. Where’s that bargaining deal? Where’s that capitalist competition?”

While Biden’s expertise and experience do not lie in business, he did highlight the importance of responsible business practices in a stable and equitable society. And perhaps, ultimately, that is the most valuable insight that he can provide to MBA students—a unique vision about business that tries to examine its role in the rest of the social world, along with profit and productivity.

This article has been edited and republished with permissions from our sister site, Clear Admit.

Boston News: Northeastern Explores Trump Tweets, MIT Offers FinTech Advice and More

Let’s explore some of the most interesting stories that have emerged from Boston metro business schools this week.

Can A Trump Tweet Dramatically Sway A Company’s Value? – Northeastern’s D’Amore-McKim Blog

Will Clark, DMSB ’17, along with Northeastern University D’Amore-McKim School of Business finance professors David Myers and Jeffery Born, sought to understand the impact that President Trump’s tweets—which often directly address publicly traded companies like Ford, Toyota, Walmart, GM, and Boeing—had on their stock market value.

“Past presidents communicated through the media. This was the first time that a president was communicating directly with the public—with investors—about companies. We really weren’t sure what to expect from the data,” says Clark, who is now a credit analyst with Morgan Stanley.

The trio’s research found that Trump’s tweets, in fact, did have some impact on companies, often increasing trade volume within the first few hours and days after he references them on the social media platform. The research was revealed in the academic journal Algorithmic Finance.

“The team found that Trump’s tweets dramatically increased trading volume for the companies’ stocks in the first few days following a tweet. They also found that positive (or negative) tweets about companies increased (or decreased) the firms’ stock prices by a modest amount—just 1 percent. But the changes were only temporary: Within a few days, the firms’ trading volumes and stock prices returned to pre-tweet levels.”

The lasting effect, however, was found to be longing. The trio notes that the most active traders, which they refer to as “noise traders,” were very reactive to Trump’s words, with trading tapering off after only a few days.

“They’re regular people and under-informed investors who want to get in and out and make a buck without thinking too long and hard about it,” Born notes about the financial impact of Trump tweets.

You can read more about the financial research on the Trump tweets from D’Amore-McKim here.

3 Lessons To Keep In Mind When Starting A FinTech Venture – MIT Sloan Newsroom

MIT Sloan School of Management MBA alum Sophia Lin, ’12, and her partner Andrew Kelley of the FinTech startup Keel, which connects “rookie investors with more seasoned ones,” shares some hard-won lessons in an op-ed for the Sloan blog. First of all: beware of hidden costs specific to FinTech. “

“Starting costs are higher than other industries because of data, infrastructure, and security requirements,” Lin said. “Data is expensive, which stops a lot of early stage startups from entering this field. But you need data to build your product.”

Read all of Lin’s words of wisdom here.

More CEOs Have Begun To Take Social Responsibility Seriously – HBR

CEOs from Facebook’s Mark Zuckerberg to Blackrock’s Larry Fink have begun to take very public stands to address the long-term impacts their products have had and continue to have on communities and the environment.

“We are witnessing a big, transitional moment—akin to the transition from analog to digital, or the realization that globalization is a really big deal. Companies are beginning to realize that paying attention to the longer term, to the perceptions of their company, and to the social consequences of their products is good business.”

Harvard Business School John and Natty McArthur University Professor Rebecca M. Henderson also explains that there are distinct differences between the size of a company, which often contrasts with the social goals of the company. The larger the company, the more long-term the outlook, she explains. Unlike small companies, larger firms worry about quarter-to-quarter results less.

“Big firms can also internalize certain externalities. An externality is a cost from a transaction that doesn’t fall on the buyer or the seller. If I pollute the air to make a product I sell to you, the cost of that pollution is spread out across society, and isn’t incorporated in the price I charge you for the product. Externalities pose problems for markets, since neither buyer nor seller have any incentive to deal with the costs. But sometimes, for really large firms, things work differently.”

The unfortunate causality, she notes, is that we are often reliant on the largest companies to take the initiative for causes that may be considered part of the global good. If some companies among the Fortune 500 elect to, say, go carbon neutral within the next decade, that can have a profound impact on other competing companies. And if those initiatives are not as profitable, there is an even greater risk of other companies being reluctant to attempt similar efforts.

Read more about the growing CSR trend among CEOs here.

These LA Business Schools Are Helping Low Income Students Pursue Their Dreams

For many low-income applicants, unfortunately, the cost of an MBA program is just out of reach. That’s because, by the time you count tuition (often upwards of $80,000), boarding and books ($40,000), and other expenditures, the average cost of an MBA is around $140,000 according to Investopedia. And that’s all before you count lost salary for two years for a full-time MBA program.

What can you do?

For low-income MBA applicants in Los Angeles, California you don’t have to give up on your dreams due to money. Instead, business schools offer many options to help pay for your MBA program.

California DREAM Act

The California DREAM Act of 2011 is currently available to California residents who attended and graduated from high school in the state and are enrolled in an accredited California Institution of Higher Education. If you meet these eligibility requirements, you’ll be given access to California State financial aid and scholarships as well as specific university financial aid programs. In addition, need-based graduate applicants are eligible for the State University Grant (SUG) program, which awards up to $7,176 to help cover tuition.

California State University’s Long Beach College of Business Administration is just one of the MBA programs that provides this type of financial aid to low-income MBA applicants. The College of Business Economics at Cal State L.A. also accepts DREAM Act Applications for student financial aid.

Scholarships

MBA scholarships for low-income applicants are one of the best ways to help pay for your degree program. Scholarships vary by school and can range from a few thousand dollars per year to full-tuition coverage plus a stipend.

At the UCLA Anderson School, there are six unique fellowships available to MBA applicants.

- Donor Fellowships are awarded to MBA applicants based on professional development, intended career, community involvement, and/or financial need.

- Merit Fellowships are awarded based on the strength of a student’s application.

- External Fellowships are available for a variety of different situations and students. One example is the Girard Miller Foundation scholarship, which is awarded to a graduate student preparing for a career in state or local government finance.

Teaching Assistantships

For California MBA students, financial aid doesn’t stop in the first year. For second-year full-time MBA students, many Los Angeles business schools offer Teaching Assistantship (TA) positions. These positions are usually awarded to students who keep their grade point averages above a certain level and who apply and receive an appointment. The award amount varies by business school but, in some cases, covers 100 percent of a student’s services fee and tuition.

At UC Irvine’s Paul Merage School of Business, full-time MBA students who gain a TA appointment receive payment for 100 percent of their Graduate Student Health Insurance Program (GSHIP) premium. They also receive 100 percent of the Student Services Fee and Tuition components per quarter.

Military Veteran Aid

For low-income MBA applicants who also have a history of military service, there are many unique financial aid opportunities. The exact services available will depend on the school, but some of these programs are available at schools across California and the U.S.

First, there’s the Yellow Ribbon Program, which many Los Angeles business schools take part in, including Chapman University Argyros School of Business. This program awards MBA students up to $6,000 for tuition and fees. Another program open to military veterans is the Post-9/11 GI Bill, which includes payments directly to the university for tuition and fees, a monthly housing allowance, and an annual books and supplies stipend up to $1,000 per year.

Individual schools like the USC Marshall School of Business also offer their own specific scholarships for military veterans. The Schoen Family Scholarship Program for Veterans is available to full-time MBA students at Marshall and has, to date, provided a staggering $1.2 million in financial support to 173 students at the university.

Loans

Finally, most low-income MBA applicants in Los Angeles are eligible for federal student loans. Direct PLUS Loans are available to graduate students to help pay for educational expenses up to the cost of attendance. MBA students can request unsubsidized loans up to their full eligibility with an Income-Driven Repayment Plan that allows you to make payments based on your adjusted gross income. In most cases, payment will begin until after graduation.

For MBA applicants at Pepperdine University’s Graziadio School of Business and Management, financial aid loan application for Federal Graduate PLUS student aid and Federal Direct Stafford Loans is easy. The school provides loan counseling for graduate student borrowers, loan calculators, and more.

For more information about how your business school could help cover the cost of your MBA program, visit your school website and contact their financial aid office. Scholarships, loans, and aid opportunities vary per school. The Simple Dollar also has a handy guide on how DACA recipients may be able to handle financial expectations for students around the U.S.

2018 Trends: New York City’s MBA Future

It doesn’t take a stable genius™ to figure out that New York City is the world’s most highly sought-after 22.82 mi² strip of land to pursue an MBA.

As is the case with most prime real estate, the stakes are high and the competition fierce. For many prospective business schoolers, the decision to step into the gauntlet is one made with a healthy sort of trepidation.

Hefty price tags and cutthroat admissions present real barriers for prospective students and deter more than a few. Still, many equate the New York MBA experience to a dream scenario—or a Gordon Gecko-style fantasy, replete with the promise of a staggering salary, an attractive range of employment opportunities, and prime placement in a city of constant progress.

How does the dream stack up to reality? Schools weigh in on 2017 trends for graduates, many of whom report satisfaction with employment offers. Let’s take a look at how MBA graduates are getting the most of their newly minted degrees!

2018 New York City MBA Trends

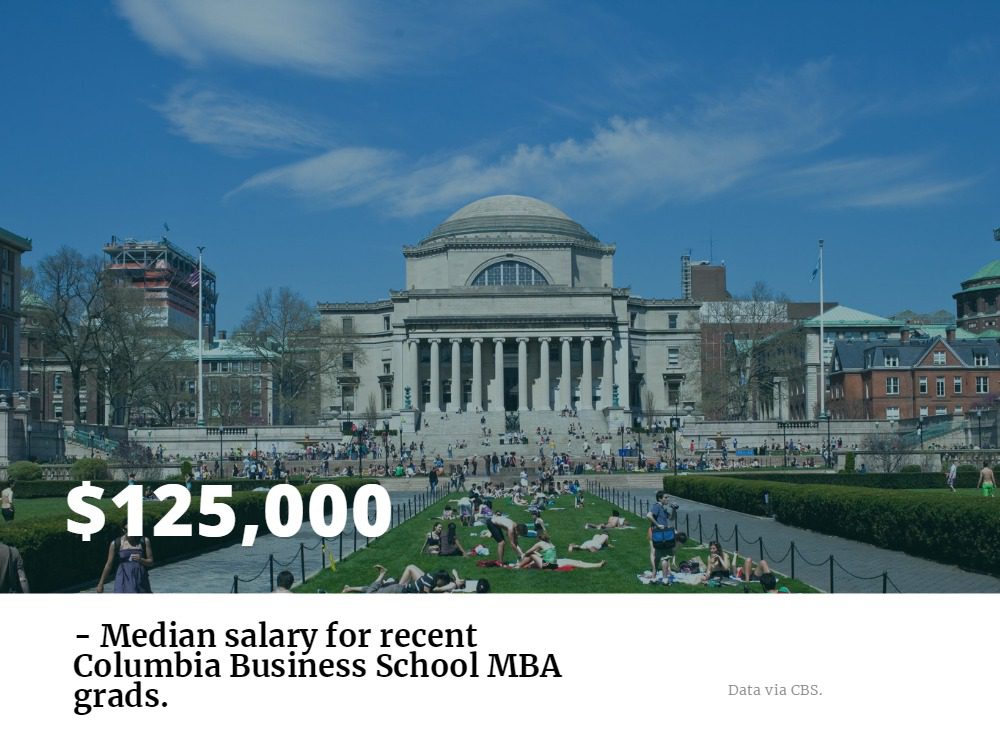

Columbia Business School

According to the school’s most recent MBA employment report, less than 2 percent of Columbia Business School graduates reported salary as the primary reason for accepting an offer. While the honestly of that polling answer pool is debatable, Columbia School of Business is the king when it comes to starting salaries on our list, with median salary of $125,000. Of the graduating class, 93.2 percent of students accepted employment offers within three months. Approximately 28 of 1,019 total students stepped aside to create their own companies. Per the standard with many of the NY-area schools, the largest portion of graduates selected financial services (34.4 percent) as their field of choice, followed closely by consulting (33.1 percent) and media and technology (15.6 percent). Companies such as McKinsey & Company, Amazon, Goldman, Sachs & Co., and Morgan Stanley welcomed a majority of Columbia’s finest.

The boastful salary expectations, unsurprisingly, are tempered a bit by the costs of the CBS MBA program. The current estimated budget for Columbia MBAs comes in at $107,749 in the first year, of which includes over $21,000 for room and board. Tuition in isolation, however, costs $71,544 for the first year. Looking at a degree at any New York City school, never mind an Ivy League institution, means cost of living has to be taken in heavy consideration, which can vary greatly from borough to borough.

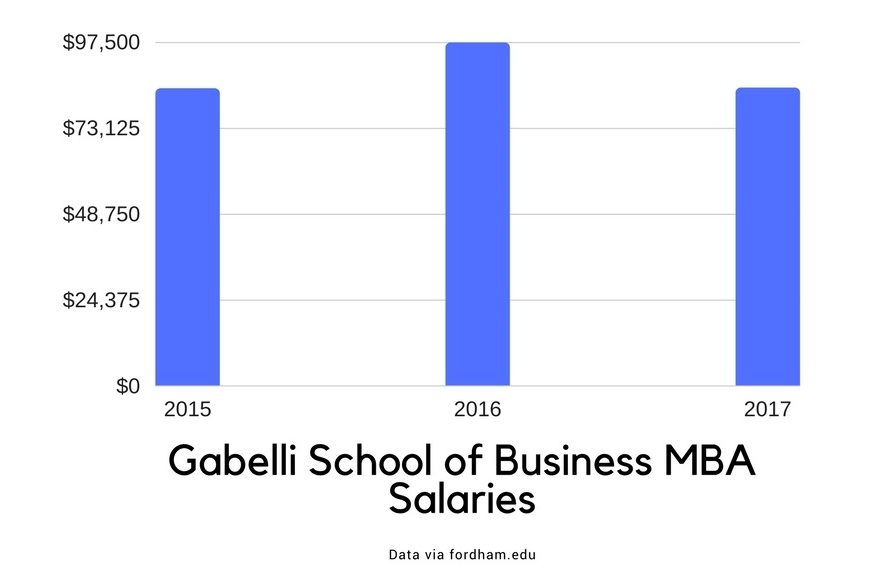

Fordham University’s Gabelli School of Business

About 88 percent of students in the Fordham Gabelli School of Business graduating class accepted employment offers within six months after graduation. Starting salary rates were below Columbia’s, at an average of $84,593, with an average signing bonus of $15,536 and additional compensation of $14,510. That average salary figure is an approximate 13 percent drop from the previous year’s reported averages.

Out of the many fields MBA students typically chose this year, Fordham students favored less predictable fields: just under 50 percent went into financial services, while 11 percent earning employment in consumer products, technology, and media, respectively. Unlike MBA graduates from many other NYC schools, however, only 5 percent of Gabelli students went into consulting, signifying a deeper trend of tech continuing its encroachment on MBA talent.

Compared to many other schools on this list, Gabelli’s distinct advantage is cost. The first year of the MBA program currently costs $49,645: more than 30 percent less than the cost of the Columbia full-time MBA tuition.

NYU Stern School of Business

This may shock you, but, NYU Stern MBA students are doing pretty well, with an average starting salary of $121,146 in placement of some of the most prestigious institutions in finance (32.4 percent), consulting (26 percent), technology (16.8 percent), real estate (3.5 percent), and retail (3.2 percent). Around 83 percent of those students landed jobs in the Northeast U.S., while nearly 10 percent of graduates found positions in Asia, Europe, and South America. Nearly half of all job offers were the result of an internship facilitated by NYU.

Like the trend at Gabelli, NYU grads jumping into tech has been steadily climbing over the past few years, rising from just 6 percent of employed grads from the Class of 2014, to 17 percent for the most recent class. The incremental increase coincides with the school’s recently added Tech MBA.

Stevens Institute of Technology School of Business

In a metro brimming with very successful business schools, the Stevens Institute of Technology School of Business separates itself with an incredible employment placement rate of 94.9 percent; the best placement among all business schools in the country, according to U.S. News & World Report.

The Stevens MBA faculty claim to provide “exceptional career services much earlier than other universities.” 90 percent were employed in the industry of their choice. Starting salaries fell between $88,805—$125,000. Companies such as Goldman Sachs, Protiviti, PwC ,and Prudential offered employment opportunities for these students.

Cornell University’s SC Johnson Graduate School of Management

About 93 percent of students from Cornell‘s Ithaca and NYC campuses received employment offers within six months of graduation. The average base salary was $125,578, which was an increase from previous years “driven by salary growth in consulting and finance.” Chosen fields for students were finance (38 percent), consulting (26 percent), and general management (21 percent). Out of the 122 companies that sought 2017 graduate students, the top recruiters were Citi Group, Amazon, Deloitte Consulting LLP, Ernst & Young, and McKinsey & Company.

Even Cornell MBA students in an internship were earning some of the best salaries in the country, pulling in a reported $8,764 per month. Those figures out over a 12-month rate are more than triple the average intern salary, according to Glassdoor data.

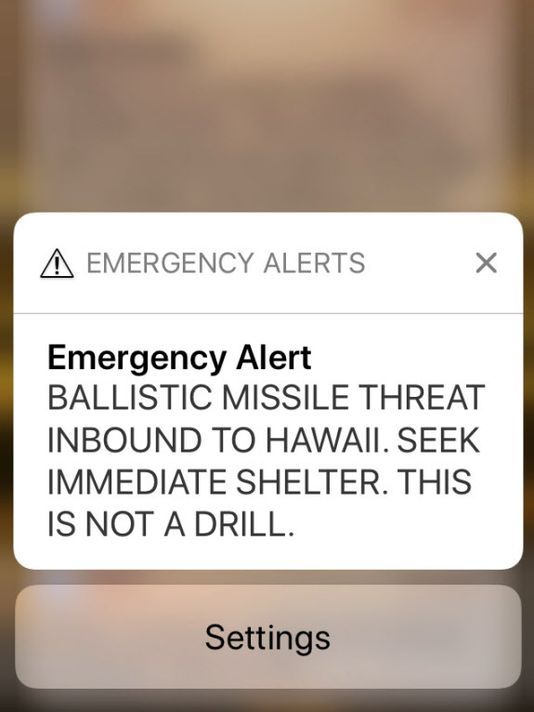

How Can We Respond To A Crisis Better? An MIT Alum Has a Few Suggestions

In the wake of Hawaii’s false emergency threat last week, MIT Sloan recently discussed the two key lessons that will make countries more “efficient when responding to a crisis.”

Miyamoto International’s Elizabeth Petheo (MBA ’14) whose career has focused on international urban disaster and risk reduction and resiliency programs believes that countries in which disasters occur should drive resiliency efforts, but “international actors can act as a catalyst for knowledge transfer.”

Petheo explains that the national actors “who know the area best, understand what capabilities their community already has, and what needs to be strengthened” are the ones who need to drive the conversation. She advises communities to develop a checklist of sorts and ensure they have firm handles on questions related to the necessary equipment, whether there’s a control structure in place to make decisions, “who else in their ecosystem will be respond to disasters, and how their specific work area impacts other areas.”

Photo via Caleb Jones/AP

Part two of disaster relief involves the perspectives—and efforts—of the international community, which are necessary for communities to “understand links—how different actors who respond in a time of crisis can help and support each other,” according to Petheo.

Miyamoto, for instance, uses data to “help local first responders understand what different scenarios would be if an earthquake did strike their area, then help communities identify the gaps in their readiness and what areas could be strengthened.”

“To prepare for a crisis, there are a number of questions that communities can ask themselves. ‘This is not an exhaustive list,’ Petheo said, ‘but there are a couple of different buckets: the logistical and operations side of things; overall administrative management of how things get executed; and the players themselves.'”

Petheo concludes, “There is the economic, societal, social, and individual impact that’s happening all at the same time, which is what makes these kinds of emergencies so complex [but] the more you can think through what possible scenarios would be, what the situation that the community or government face would be, the better they are in coping when a crisis actually happens.”

Check out the recent of MIT’s article on disaster relief here.